Published (and amended) in The New Zealand Herald, 10th. September 2022

The recent furore over the proposal to charge GST on KiwiSaver management fees shows three things. Firstly, tax remains a treacherous area for policy debate in New Zealand.

Secondly, KiwiSaver has built a strong and thriving industry of financial advisers and managers who are now in a strong position to protect their interests.

Thirdly, we now learn something that all retirement savers should have emblazoned on their accounts – that a small, early addition of cost in their retirement portfolio can translate over time, and through the magic of compound interest, into a very considerable depletion of their final savings balance.

The Financial Markets Authority (FMA), the ostensible regulator of the sector, helpfully provided modelling to support the case. It forecast that requiring all fund managers to pay 15 per cent GST on managed fund fees would see the value of the country’s KiwiSaver investments fall by 5 per cent by 2070.

This is a revealing statistic because it highlights the impact of KiwiSaver fund fees. Average fees (management and administration) on the country’s KiwiSaver balances amount to 0.8%, according to the FMA.

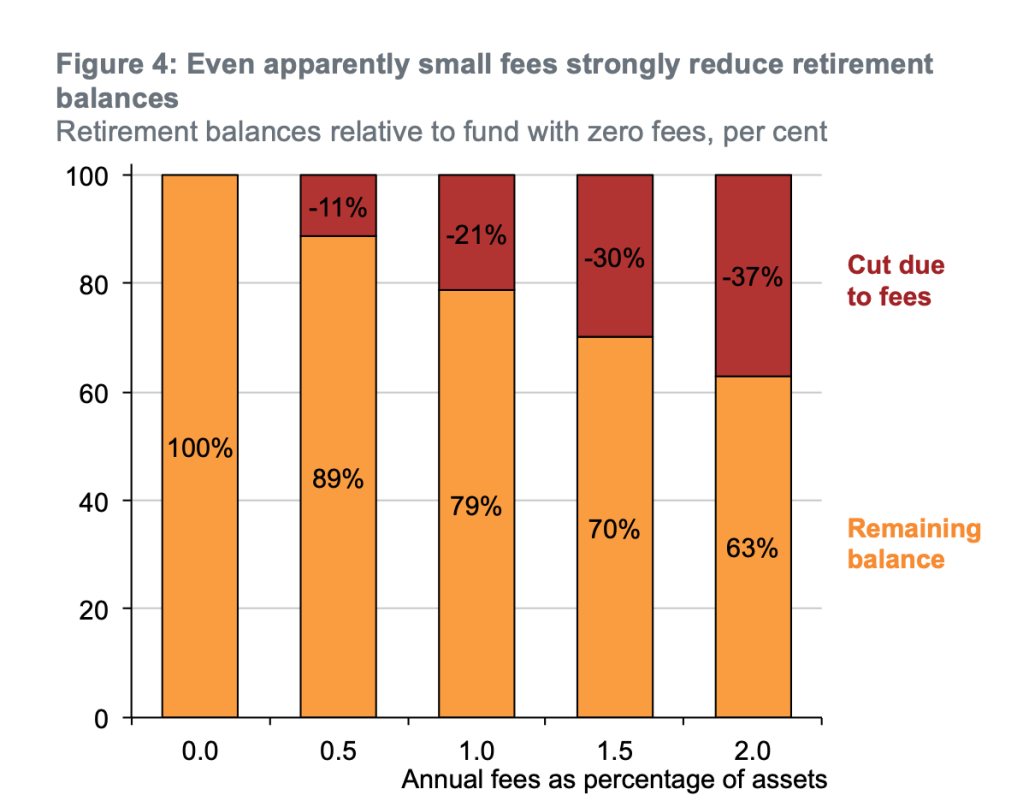

A Grattan Institute study in Australia found that over 40 years, a 1 per cent fee would reduce one’s retirement savings by a fifth. This assumes annual wage growth of 1.8 per cent and portfolio returns of 5 per cent (see figure below).

A fee of 1.5 per cent – which is is probably top of the range in New Zealand – would reduce one’s retirement balance by a third over 40 years.

At the other end of the scale, I have a retirement portfolio I started before KiwiSaver with a “no frills” non-metro investment outfit. This has grown eightfold in value in as many years, provides returns that match those of insurance industry benchmarks, and costs me 0.3 per cent annually, inclusive of GST at 15 per cent.

There is at least one KiwiSaver provider that charges at this low level (albeit without having to absorb the full level of GST).

The remarkable thing is that, according to FMA research, there is no relationship between fees and returns. In other words, the great majority of KiwiSavers are paying fees that greatly reduce their final balances, forego significant reinvestment of returns, and provide them with no apparent advantage over low-cost providers.

Other research by the FMA shows that New Zealand fees are not internationally competitive. The closest comparator to ours is the auto-enrolment retirement system in the United Kingdom. Indeed, it was largely modelled on ours. Our provider fees are anything between 30 to 75 per cent higher.

There is almost no competitive pressure on fees in New Zealand. Yes, the providers compete on advertising and offerings, but not on fees.

When a certain provider advertised their low fees as an attraction to new clients they were admonished by the FMA on the basis that there was no certainty that these fees would retain their competitive edge, and thus deliver a better retirement income over a full life cycle of saving. Also, the provider’s assumptions were not prominently disclosed.

The FMA has asked providers to reduce their fees if they are seen to be “unreasonable”. But the real pressure has come from the government’s tendering of default providers to favour those offering lower fees.

While the Australian system of contributory private provision is compulsory, they have come across a similar set of problems. Their fees are even more uncompetitive than New Zealand’s, and they have asked their Productivity Commission to consider ways of getting better value for money for superannuation clients, including compulsory tendering, underperformance tests, and merging of providers.

It is not as if the government is without leverage. It contributes almost a billion dollars a year to KiwiSaver balances. One wonders why this is not used more judiciously to encourage the ratcheting down of fees; after all, agencies like Treasury, MBIE and FMA follow an orthodox analytical model, they are cautious, and they are probably too close to the industry to do anything of this kind.

The government also has a moral obligation. The New Zealand system was – when it was established in 2007 – and still is, in many respects, world leading. Among other things, it was a pioneer in using the insights of “nudge” philosophy and behavioural economics to gain high levels of enrolment by making the system “opt out” rather than “opt in”, and having a centralised system via Inland Revenue of following clients as they cycle through different jobs.

There are ethical arguments about whether the “nudge” approach is manipulative as it shapes choices in such a way as to make enrolment almost universal. But it could be argued that the cause – saving for retirement – justifies this approach and avoids having to enforce a mandate.

Nevertheless, once people are in the system, the predominant economic model is of the rational, informed user in a competitive and fully informational market. But the reality is very different. The relationship is asymmetric and opaque to the average user, and providers are not under pressure to reduce their fees in any meaningful way.

Therefore, we need to move away from the orthodox approach of “caveat emptor” to one that takes greater care to re-balance the system in the client’s favour, particularly for low-income savers.

The government could tender for default KiwiSaver providers more frequently. It could use its contributions to the scheme to incentivise providers to lower fees. The Super Fund could even join the market to provide more competition. And savers could be offered better chances to switch.

Peter Davis, Emeritus Professor in Population Health and Social Science, University of Auckland.

Discover more from Peter Davis NZ

Subscribe to get the latest posts sent to your email.

Well said Peter. Very informative as usual. Keep up the good work. I always enjoy your articles.

LikeLike

Thank you. I try my best!

LikeLike

Thank you. I try my best. Unfortunately it is a little too much like being a voice in the wilderness.

LikeLike

Excellent piece, Peter – many thanks for the links to the two FMA reports. Notably my Kiwisaver provider has not made them available. Grateful for your analysis.

LikeLike

Thank you. Yes, the industry has a very nice thing going here and nobody – not the regulatory authorities, not the government, not the experts, not the media – is telling the poor old saver about how rigged the system is.

I only worked this out over the years. Thirty years ago I was introduced to the NZX index funds that just track different asset classes and require no intermediary. That was my introduction to the whole concept that passive investing – rather than stock picking – was a reasonable investment strategy. Then about ten years ago I came across a columnist in the Herald who was a contrarian and a kind of “whistle blower” on the industry, and I joined his investment firm (which matches all the necessary returns and charges low fees). Finally, I came across these reports from an OZ think tank – the Grattan Institute – that applied all the necessary analytical skills to the OZ system, which is riddled with shortcomings, and it is from there that I was able to derive standard measures of the drawdown on final balances from fees. And of course the FMA report confirmed that there is no relationship between fees and returns, and that we pay higher fees than in the UK system – and does absolutely nothing about it. Indeed, it admonished the one KiwiSaver that does have low fees – Simplicity – for skiting about this. Yet it allows other firms that charge high fees to make all sorts of misleading claims about their merits. The system is rigged and the guardians are doing nothing.

This is little old me with no background in this area, and nobody, absolutely nobody, is taking on the industry in any meaningful way to protect the long-term retirement interests of the saver.

LikeLike

Well, that is heinous. Essentially the FMA is not doing its job.

Kiwi Wealth (my provider) has just been sold and from the FMA data my fees will go up. No one has explained this (although I explicitly asked KiwiWealth when the sale was announced and received the fob off answer along the lines that information was forthcoming. Needless to say it has not arrived yet.) This looks very much to me like the FMA being too cosy with the sector and consequently not doing its job. As you say, telling off a provider whose fees are low is not putting savers first!

LikeLike

The government should have bought KiwiWealth along with the bank, and then used it as a way of bringing fees down in the sector!

LikeLike

Yes, I think the FMA is too close to the industry, and the system is set up in a way that does not protect savers’ long-term interests. It is part and parcel of a conventional and orthodox economic model that the government cannot buck and that does not serve us well.

LikeLike

I gave up on managed funds of any sort years ago when I figured out how much I was losing to feed. I asked a few providers, including Gareth Morgan, whether they could link their fees to returns. Their reply? We wouldn’t make enough money.

LikeLike

And yet the Super Fund has the equivalent of fees at .3% – which is the rate of Simplicity and my provider – and returns of 10% steadily, over a period of 20 years.

The problem is the term “managed”. Many such programems rely heavily not on active management but passive, indexed representations of the market, with judicious interventions to avoid the worst; this allows them to keep their fees low and net returns high. Once you have active management with people who think they can beat the market – which they can’t – you are inevitably up for high fees, and inevitably again the returns cannot match those fees. That would be the kernel of truth in Gareth Morgan’s comment.

But once you give up on the hubris of beating the market – not just now and then but all the time – then you can have a solid passive funding base, with some stock picking; and the fees can be much lower. The returns are no different (as shown by the FMA report), but the fees are lower so that you build a retirement future on that.

LikeLiked by 1 person

Thanks. This is something I have stumbled on and learned about over a period of time, otherwise I would be in the same boat as other savers. We are just not well served by so-called advisers (most of whom have conflicts of interest), by the industry (which has no interest in savers knowing about this), by the media (who are also conflicted and strangely allergic to helping savers understand this better), and, worst of all, the regulatory authorities that adhere to a very orthodox, hands-off model and are probably too close to the industry anyway.

Thirty years ago I found out about NZX index funds, and through that I discovered you could get perfectly good returns without having to work through an intermediary. Then I came across a Herald columnist who was an advocate for low fees, and I have joined his financial advisory outfit as a saver – and, as mentioned in the article, I pay at the lowest level of KiwiSaver, including full 15% GST, and returns match those of standard pension scheme benchmarks. I also followed an Australian think tank that outlined the problems with their system, including high fees, lack of competition, and too many breaks for affluence savers.

Then along came this almost completely manufactured GST furore, and it all fell into place as to how the industry was keeping very quiet about fees and making us all think that it was all about GST (which I understand the industry is non-compliant on). Unfortunately, I doubt whether anything will change, at least in the near future, because the waters have been so successfully muddied by the industry, and because the major political parties have backed themselves into oppositional stances when actually they both have an interest in savers being protected!

LikeLike

Very well said Peter. The cost of so-called managed funds has been an iniquitous impost on savers for generations of Kiwis without most people even realizing.

Good on you for calling this out, long past time for us to have this conversation.

LikeLike