Published (and amended) in The New Zealand Herald, 5th. January 2023

It is just over 15 years since, on 2nd. July 2007, KiwiSaver, New Zealand’s auto-enrol, work-based retirement savings scheme, officially started.

How has it fared? Over three million people are enrolled, close to the size of the active workforce. Funds to the value of $90 billion are being managed, equivalent to nearly a quarter of the country’s GDP. It has stimulated the financial sector. And the initiative has drawn international interest, with the United Kingdom (UK) introducing a very similar scheme.

Are there any downsides? There are several. First, a third to a half of those officially enrolled are not actually contributing. Second, the average holding is under $30,000, which, even allowing for non-contributors and youthful savers, cannot generate an adequate retirement income, and under current policy settings it is hard to see this changing.

Furthermore, according to a review in the early years of the scheme: KiwiSaver added about a third to existing savings; those saving were not necessarily anticipating a shortfall in retirement and, indeed, a quarter of Crown subsidies went to the top income quartile, who also accounted for nearly half of savings; there was no evidence of net wealth accumulation; and, for each dollar of Crown subsidy, additional savings were between $0.20 and $0.38.

Finally, the system of converting investment returns into final retirement savings is very inefficient. The annual average fee being charged by KiwiSaver providers is about one per cent of holdings. To the novice saver this may not sound a lot, but it is likely to translate into a shortfall of 20-30 per cent in final savings. In other words, compounding that small fee percentage over a lifetime of saving translates into a very considerable depletion of final retirement funds.

This fee level is in some instances almost double that in the comparable system in the UK. By comparison the New Zealand Super Fund has reported annual costs of around 0.3% over the last ten years with annual returns of about 10%. Some KiwiSaver providers are able to match that fee level, with good returns, but at the other extreme are providers charging 1.5% and more. This impression of an uncompetitive market is reinforced by the sheer number of providers (nearly 40), suggesting current margins allow many small players to thrive while charging high fees.

The Financial Markets Authority (FMA), the ostensible regulator of the sector, confirms that all is not well with the competitive playing field in the KiwiSaver sector. In a number of reports it has found the following:

- Where scale (i.e. size) of a KiwiSaver provider exists, its benefits are typically not shared with members.

- There is no systematic relationship between fees charged and returns received.

- There is no systematic relationship between fees charged and degree of active management.

- Active funds – that is, funds that use a stock selection rather than a passive, tracking approach – typically do not outperform their market index after fees.

- Fund managers are often not using an appropriate market index or benchmark for judging their fund’s performance

- Managers commonly pay commission to third parties for new customers, without adequate disclosure.

- The FMA’s KiwiSaver Tracker shows a range of 20-30% investment returns going to fees.

Do these supposed shortcomings matter? After all, New Zealand has had mixed success when it comes to encouraging competition in key markets, so maybe KiwiSaver is no different. While there seem to be some wins in the telecommunications market, the Government had to intervene to move the Commerce Commission along in the supermarket sector, and there remain major doubts about the effectiveness of competition in the electricity market. By contrast the public pressure for intervention with KiwiSaver is minimal, although the Australian Government felt bound to ask its productivity commission to investigate efficiency and competitiveness in its (compulsory) superannuation scheme after years of pressure and complaints. Among other things that inquiry identified high fees as an issue.

So, there is a prima facie argument for a review on grounds of competition and efficiency alone. But there is also a moral case. KiwiSaver has been world-leading in introducing a retirement scheme that, while it is ostensibly voluntary, operates a form of “soft compulsion” by making it easy for people to join and hard to leave by shaping their choice architecture. Given that, there is an argument that novice savers entering the scheme should not be left to an asymmetric and opaque market of savvy financial providers. After all, if the saver’s choice architecture has been massaged (for good policy reasons), then arguably so should that of the financial provider!

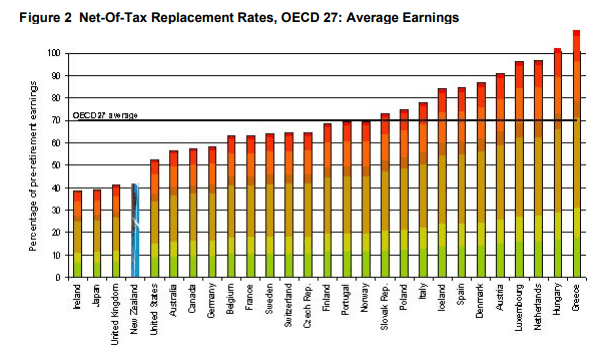

There is also the issue that, even under current policy settings with KiwiSaver as an adjunct to National Superannuation, the overall income replacement rate at retirement for New Zealanders at and below the average wage is only 40%, among the lowest in the OECD. Indeed, the main beneficiaries from the scheme seem to be middle- and higher-income owners (since they are able to reach target retirement savings more rapidly because of their higher incomes).

There are then good reasons for a review of KiwiSaver – on grounds of lack of price competition and inefficiency in generating adequate final retirement savings, because of the institutional asymmetry between saver and provider that is embedded in the programme, and on account of a fundamental policy shortcoming in its failure to help New Zealanders who are solely reliant on National Superannuation to better prepare for a more comfortable retirement.

After fifteen years, time for a review?

Peter Davis, Chair, The Helen Clark Foundation, an independent public policy think tank.

Discover more from Peter Davis NZ

Subscribe to get the latest posts sent to your email.

Very eloquently written and understandable to the average retail investor, I think and thank you for that.

This is a huge issue and the only KS fund I am aware that is meaningfully reducing fees as it grows is Simplicity, with its passive strategy. Perhaps you have identified others in your research?

LikeLike

The failure lies in the economic model used and the role of government in setting the parameters. There is no meaningful price competition, despite the economic model claiming that this is possible, and the relevant regulatory authority (FMA) simply does not have the tools, courage or the intellectual fire-power to intervene. This is the kind of area an outfit like the Commerce Commission could have a role, but more particularly the government since retirement incomes are a social good in most respects. The troubling thing about Simplicity is that they were disciplined for claiming that they were better value because their fees were lower. Doubtless the FMA was under pressure from the finance sector which is on a gravy train and doesn’t want anybody talking about fee levels!

LikeLike

I didn’t enter Kiwisaver because I discovered relatively early (only took me 15 years!) that the fees charged on managed saving schemes in NZ are usurious … my money increased by the rate of inflation, at best, in 3 different (reputable) schemes. I was told I had invested at the wrong time, in the wrong things. I hadn’t. In fact, when I asked what I should have invested in they told me, and that was where I had been invested! In one example they said I would have received 30% returns over 3 years. I said I had received 10%. The advisor said, well there’s tax, that removed 10%. “What happened to the other 10%?”, I asked. “I don’t know,” was his reply. I know – it was their fees. He was either incompetent, or a liar. Not awe inspiring.

… in the end, I told them I would have more fun losing my own money. I went to Gareth Morgan and asked, how about a scheme where I paid a fee that was a proportion of the INCREASE in my funds c.f. a proportion of the funds themselves. He told me that it would not be profitable enough to operate. That says a lot! So good luck on government reforming the sector. They might not want to operate if their returns are reduced.

However, bigger picture, is expecting a return on money simply because you have it wrong altogether? It increases the divide between wealthy and poor and the degree of distance between saver and where the funds are invested makes it impossible to ensure that funds are really used for good (whatever green or ethical investment wash is put on a fund). Doesn’t this perpetuate the unsustainable growth model, suggesting that your money can grow indefinitely, which means something else has to grow indefinitely also, which is impossible in a finite world?

LikeLike

The NZ finance industry is on a gravy train with KiwiSaver. This is unfortunate because basically it is a sound idea that we should set aside for retirement through contributory schemes rather than just dip into the tax system as with National Super (which in the long run is unviable as the demographics of our country shift). The settings for KiwiSaver are such that there is no pressure to reduce fees (i.e. no price competition). I have a retirement portfolio that is outside KiwiSaver (I started before KS was established), and I get returns that match standard pension schemes, paying 0.3% of assets, which is a third of the average charged by KS providers. Let that sink in. I have a common-or-garden no-frills provincial outfit that provides me with returns matching standard pensions schemes (about 5% cash income on assets deployed), yet I pay a third of the AVERAGE charge across the fully professional KS sector. Nine of the top KS providers are bank outfits. They are creaming it, and there is fundamentally no effective restraint on this given the current economic model of the sovereign consumer and saver (up against savvy providers). The media are complicit, as are most commentators, and of course nobody in the industry is going to own up. And the universities are no help. It is kind of scandalous!

LikeLike

The NZ are creaming it but I still think two fundamental questions remain unanswered:

1) Why should the industry charge a percentage of ASSETS at all. Why not a percentage of performance? Then you could take away the need for government regulation. Schemes that don’t provide decent returns won’t exist.

2) Is it right for people to increase the amount of money they have simply because they have it? Isn’t this a huge driver of the wealthy/poor divide. The better returns those with money have, the greater that divide will be?

LikeLike

On the first point, you are right. But there is insufficient competition in the industry and people are on their own in dealing with it. If you look at the Super Fund, they evaluate their performance against a standard, as does my retirement investment outfit. But it is very easy for finance companies to select standards that always show them in a good light. On your second point. You are talking about a fundamental aspect of our unequal society, and really the only practical counterweight is progressive taxation and the taxation of wealth and capital gains. But those are hard to sustain against substantial push-back.

LikeLike